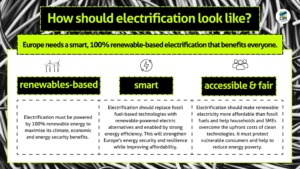

Electrification can be a powerful driver for Europe to achieve an affordable, secure and sustainable energy supply, but it needs to be smart and fair. Fulfilling its full potential will require electrification going hand in hand with increasing energy savings and rapidly deploying renewable energy. This is essential in keeping electricity growth in check, lowering overall energy demand and ensuring that electricity demand is fully met by renewable energy, rapidly decarbonising the EU’s energy system and reducing dependency on fossil fuel imports.

Ahead of the publication of the EU Electrification Action Plan, our policy experts have answered some of the pressing questions on electrification and where it fits in the EU’s overall energy transition:

-

Electrification is the replacement of technologies and processes that use fossil fuels, such as coal, oil, fossil gas, with electrically-powered equivalents. This could mean replacing a gas stove with an induction stove, replacing fossil boilers with heat pumps, a petrol car with an electric vehicle or using electric arc furnaces instead of coal-powered blast furnaces in steelmaking.

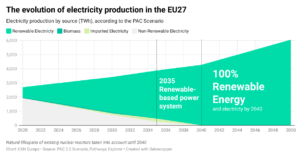

The Paris Agreement Compatible (PAC) scenario demonstrates that an energy transition that leads to climate neutrality by 2040 is both feasible and highly desirable from a climate and economic perspective, while providing co-benefits of 1 trillion euros. The scenario foresees a requirement to strongly reduce energy demand and to ramp up our production of renewable electricity as we electrify demand, reaching 100% renewable power by 2040. The scenario phases out the use of coal by 2030, fossil gas by 2035, and oil by 2040, to ensure new electricity is not supplied by fossil fuels.

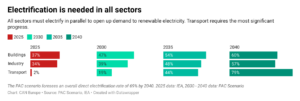

As part of the solution to phase-out other fossil-fuels from our energy system, the PAC scenario foresees a direct electrification rate of 43% by 2030 relative to final energy consumption, rising to 69% by 2040. The model breaks down the sectoral needs, showing the need to ramp up electrification in buildings, transport and industry, discussed later below.

Energy efficiency is the foundation of smart electrification and a key enabler of rapid uptake. While electrification is widely recognised as a key driver of energy efficiency, the reverse is equally true: energy efficiency is fundamental to accelerating electrification and reducing its costs. By lowering overall energy demand, energy efficiency makes it easier and more affordable to electrify buildings, transport and industry, reducing the need for costly investments in electricity generation and network infrastructure while helping to keep energy bills under control.

Strengthening energy efficiency is therefore essential to delivering an energy transition that improves people’s quality of life, particularly for vulnerable households and tackling energy poverty, while helping to achieve Europe’s energy security and ending fossil fuel dependence.

The EU already has a solid legislative framework to drive this transition through the Energy Efficiency Directive (EED), the Energy Performance of Buildings Directive (EPBD) and the Ecodesign framework. Together, these instruments provide the foundations for smarter, faster and more affordable electrification. Measures such as Zero-Emission Buildings, EV-ready infrastructure, solar-ready buildings provisions and requirements for modern technical building systems all help accelerate the uptake of electrified technologies, including heat pumps, rooftop solar and smart energy management. With the transposition deadlines for the EED and EPBD now passed, the priority must be their full and effective implementation to enable and accelerate smart electrification.

However, electrification alone will not drive energy savings. If electric technology is not more efficient than the technology based on fossil fuel it replaces, total energy consumption will not be reduced.

And electrification does not mean getting rid of fossil fuels per se as electricity power production is still dependent on fossil fuels in many countries. The continued use of coal-fired power plants and gas turbines risks high prices and could stall electrification. Electrification needs to be based on renewables.

An electrification-only approach, without ensuring a strong regulatory and market framework for ambitious energy savings, renewable energy deployment at speed and scale, and a clear fossil fuel phase-out strategy, risks a more expensive, less resilient and less effective transition, slowing emissions reductions, prolonging fossil fuel dependence and preventing Europe from taking control of its own energy future. Because it risks:

- Electricity demand that outpaces renewables supply capacity, increasing reliance on fossil fuel generation and prolonging locking in;

- Cost overruns from oversized infrastructure;

- Failure to reduce non-electric fossil fuel use.

The electrification of the European Union or an individual country is measured by taking the level of final energy demand satisfied by electricity, without taking into consideration the source of that electricity (renewable, fossil or nuclear, it is all electricity).

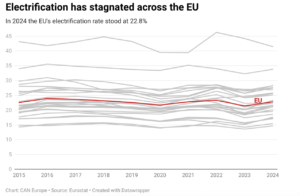

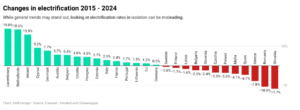

The electrification of the European Union or an individual country is measured by taking the level of final energy demand satisfied by electricity, without taking into consideration the source of that electricity (renewable, fossil or nuclear, it is all electricity).Extrapolating data from Eurostat, we can see the trend of all 27 countries, and the EU average, which shows stagnated in the rate of electrification since 2015. While the increase of renewable power has been significant in the last decade to decarbonise the electricity we use and phase out fossil fuels (in particular, coal), we have not been increasing our electricity consumption to sectors currently reliant on non-electricity fossil fuels, such as burning fossil gas directly. At the EU level, the electrification rate has hovered around 22-23%. The Commission has already set out an indicative electrification objective, referred to as a performance indicator, of 32% by 2030 launched under the Clean Industrial Deal and the Affordable Energy Action Plan.

Due to a stagnant electrification across most of Europe, it can be hard to pull out best case countries. The chart below shows the change of the share of electrification from 2015 to 2024 by each country. Some notable examples can help demonstrate the difficulty of using this metric in isolation. Take Spain, which has been championed for its use of wind and solar to decarbonise and decouple prices from gas. The country shows a slightly lower electrification rate. On the other hand, we see Ireland having a high positive change in electrification, however rather than this being due to the deployment of heat pumps and EVs, this is more likely due to the higher use of electricity for data centres. This chart demonstrates why a Union-wide, or even national economy-wide electrification targets, can be overly simplistic, and require sector-level KPIs to accurately track how demand is being electrified, and how renewable power can support decarbonisation.

Renewables-based, smart electrification relies on the deployment of new renewable generation, the setting of clear phase-out dates for fossil fuels, and the collaboration between energy efficiency and electrification. As demand is electrified, Europe will seek an increase in electricity consumption, while overall energy usage falls. There is a risk that countries may unwisely choose to prolong the life of coal-fired power plants or construct new gas-fired turbines to supply this electricity. A pathway reliant on elements of fossil-based electrification would greatly limit the greenhouse emissions reduction, and keep electricity prices linked to volatile global markets.

Renewables-based, smart electrification relies on the deployment of new renewable generation, the setting of clear phase-out dates for fossil fuels, and the collaboration between energy efficiency and electrification. As demand is electrified, Europe will seek an increase in electricity consumption, while overall energy usage falls. There is a risk that countries may unwisely choose to prolong the life of coal-fired power plants or construct new gas-fired turbines to supply this electricity. A pathway reliant on elements of fossil-based electrification would greatly limit the greenhouse emissions reduction, and keep electricity prices linked to volatile global markets.For this reason, it is essential to establish a framework for phasing out fossil fuels and their subsidies and support the deployment of renewable generation and energy demand reduction.

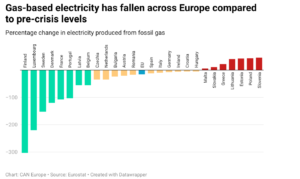

In general, EU countries have seen a reduction in the use of gas for electricity compared to pre-crisis levels (average 2017-2021 prices). However, many Member States have seen little reduction, while others have unfortunately seen an increase. This has taken place during a time of electrification stagnation, highlighting the risk that some countries may pivot back to gas as demand electrifies.

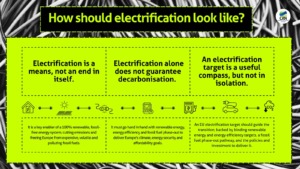

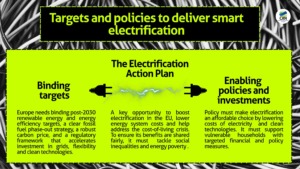

Electrification target is a useful compass, but must be underpinned with binding targets for renewable energy and energy savings. An electrification target can be a useful indicator to set the direction of travel and track progress towards a fossil-free economy. But a single headline figure in isolation cannot become the objective in itself.

Electrification target is a useful compass, but must be underpinned with binding targets for renewable energy and energy savings. An electrification target can be a useful indicator to set the direction of travel and track progress towards a fossil-free economy. But a single headline figure in isolation cannot become the objective in itself.An electrification target says little about the quality of the transition. It does not tell us whether electricity is generated from renewable energy or fossil fuels, whether energy demand is becoming more efficient, or how households and businesses can afford to electrify. Nor does it identify the policies needed to accelerate electrification across different sectors.

Rather than focusing on a single percentage, the EU should focus on what it takes to deliver smart, renewable-based electrification. This means translating any EU-wide indicator into clear sectoral pathways for buildings, transport and industry, uptake of key electrification technologies, such as heat pumps, electric vehicles and other appliances, supported by the right mix of policies and investment.

The Governance Regulation should embed smart electrification as one of the key energy transition indicators to monitor Member States’ progress, alongside with a set of KPIs including electricity-to-gas price ratio, the uptake of electrification technologies, an EU non-fossil flexibility objective/target, a KPI on increasing capacity of the existing electricity network including through the use of grid enhancing technologies and batteries-as-a-transition-asset, and targets and KPIs on acquiring system inertia.

A smart electrification framework should therefore be underpinned by:

- binding EU and national targets for renewable energy and energy efficiency

- a clear pathway to phase out fossil fuels and their subsidies

- measures to make electricity more affordable than fossil fuels through taxation and levy reform

- strong and predictable carbon pricing

- investment in grids, storage and demand side flexibility

- targeted financing and technical assistance to help households, in particular vulnerable and low-income, businesses and industry to electrify.

As Michael Liebreich and others have pointed out, designing a meaningful electrification target with a percentage is far from straightforward, with a percentage of final energy consumption as a metric. The real value of an electrification target lies not in the number itself, but in actions to drive the right investment decisions with strong markets signals (such as fossil gas boiler phase out), financing or support programs to help with upfront costs ( especially for vulnerable and low-income households), and policy reforms (electricity taxation) needed to accelerate a renewable-based, fossil-free energy system.

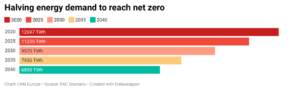

CAN Europe’s Paris Agreement Compatible Energy Scenario shows a direct electrification rate of 69% by 2040 and demonstrates at the same time that the fastest way to increase the electrification rate means lowering the overall energy demand at the same time, leading to halving energy demand by 2040, which helps making the objective easier to reach.

As mentioned above, ignoring sector specific tracking of electrification can lead to perverse incentives to reach a union-wide or national electrification figure, such as ignoring the use of energy efficiency and incentivising the use of electricity on the deployment of data centres before decarbonising the existing economy and allowing households and businesses to benefit from affordable renewable power.

As mentioned above, ignoring sector specific tracking of electrification can lead to perverse incentives to reach a union-wide or national electrification figure, such as ignoring the use of energy efficiency and incentivising the use of electricity on the deployment of data centres before decarbonising the existing economy and allowing households and businesses to benefit from affordable renewable power.Additionally, each sector needs to be treated differently. Data from the Paris Agreement Compatible (PAC) scenario shows that the trajectory of the three key sectors, industry, transport, and buildings, differs greatly, due to the requirement to deploy and integrate different technologies, and surrounding social factors. Transport for example sees some of the highest levels of electrification, but starts from a very low position. Without looking sector by sector, a country could, for example, see the risk of households and transport electrifying while their industry stays hooked to expensive, polluting fossil fuels. They may hit their national target, but risk their industry being left behind, harming competitiveness. Alternatively, a country could pour subsidies into industrial electrification while households remain vulnerable to the price swings of the global gas market. All three sectors must electrify in parallel.

Sectoral targeting will also help in the identification and filling of financial gaps. The I4CE notes that there is a 36 billion euro gap in meeting 50 million heat pump units by 2030, whereas the EU decarbonisation of transport (primarily via electrification) will require 198 billion euros per year until 2030.